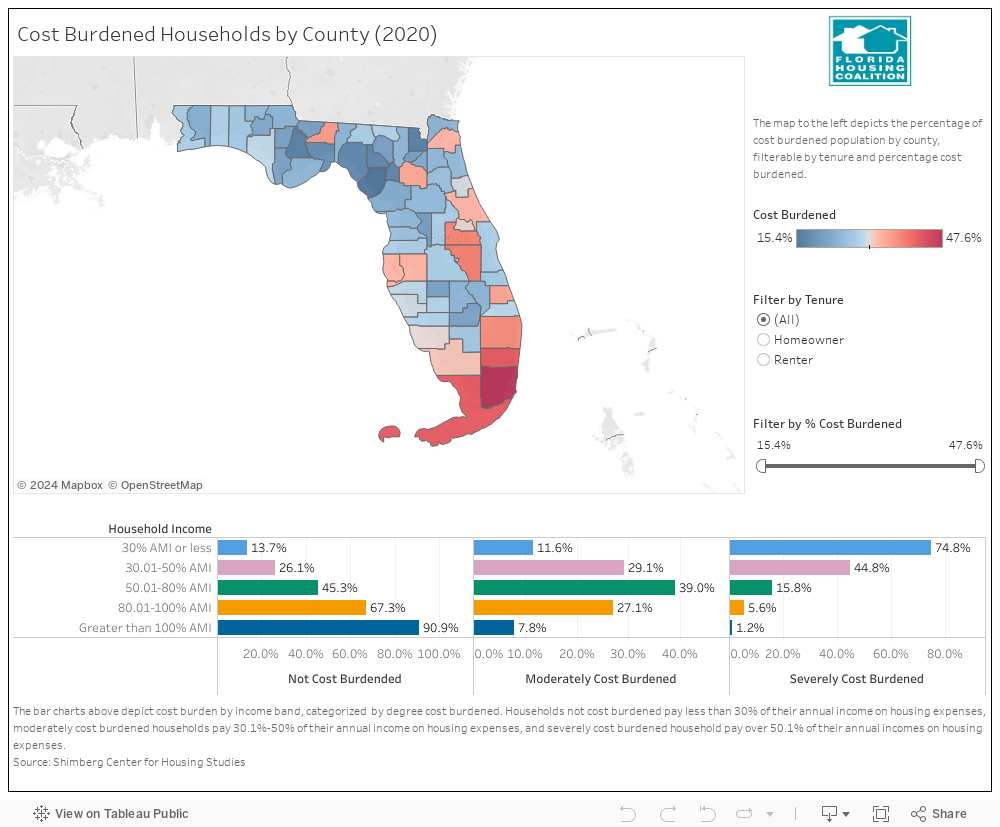

Cost Burden by County shows the distribution of cost-burdened households by income bracket and tenure in Florida. Not surprisingly, the share of cost-burdened households for each tenure type increases as income decreases. In the extremely low-income (ELI) and very low-income brackets (VLI), 86% and 74% of all households are cost-burdened, respectively, a dramatic increase from 77% and 70% in 2019. Cost burden is especially widespread among low-income renters. When filtering cost-burdened households by tenure, rates for renters consistently place at and above 40% across Florida’s counties, save for a few more rural counties.